Powerpay COVID-19 Central

Use this page as your source for any updates. They will be posted as soon as information becomes available.

Latest Updates

As a COVID-19 relief measure, the Canada Revenue Agency announced in March 2020 that it would not be sending new federal garnishment (RTP) orders to employers and advised that withholdings and payments on existing federal garnishment orders were not required, until further notice.

CRA has now confirmed that these orders will be resumed.

Any employer who needs to resume RTP deductions will be issued new RTP orders by CRA that confirm what is required. Employers are to wait for the orders to be issued. CRA’s re-issuance effort started on February 15, 2021.Additional details are available here: CRA RTP.

If you need to setup a new federal garnishment, the instructions can be found here: Set up a new garnishment

Some employers have received a letter from CRA advising of a 2020 credit on their account based on a recalculation of the 10% Temporary Wage Subsidy (TWS). At this time, Ceridian is not processing adjustments in response to those letters.

The CRA letters relate to the 2020 tax year. It is understood that 2020 credits cannot be applied to reduce 2021 source deductions.

Ceridian has been in consultation with CRA. We understand that CRA will be processing 2020 T4s before considering the distribution of any remaining credits.

The federal government in its Fall Economic Statement 2020 advised that the Canada Revenue Agency (CRA) will allow people working from home in 2020 due to COVID-19 to claim up to $400.00 for modest expenses without requiring detailed expense documentation or a completed T2200 signed by their employer.

The deduction available is based on the amount of time spent working from home.

For clarity, it is not necessary for employers to complete the T2200 form for the workers described above. The usual process for completing the T2200 form will remain available to those employees who were normally required to work away from the employer’s place of business and had to pay expenses to earn employment income.

Further details will be communicated by the CRA in the coming weeks.

With the COVID-19 situation rising in several provinces, and the changing restrictions within regions, we are reminding all customers to ensure that if you receive a package via courier that your delivery address is up to date with Ceridian.

If you require changes to your delivery address and your payroll has not been submitted, please contact your Service Delivery Team to update.

If your payroll is to process on the same day you make the request, we can attempt to change the delivery address, however there is no guarantee. Our print locations are seeing an unprecedented number of requests to intercept before delivery and will do them at best efforts.

Standard delivery practices are as follows:

- Purolator: The established delivery protocol is an automatic 2nd delivery attempt followed by the shipment to be held at the closest depot. If it remains unclaimed then it is returned to the closest Ceridian office as noted on the coverpage. Please contact Purolator to determine what depot your payroll will be held at.

- For any other couriers please contact your Service Delivery Team.

If you are unable to pick up your package from the Purolator depot and require a package to be redirected to an alternate address within the 5 day period after the payroll has processed, you will be charged a $50 one-time fee and may experience a multi-day delivery delay.

Any packages that are not picked up from the depot and returned to Ceridian may incur an additional delivery fee.

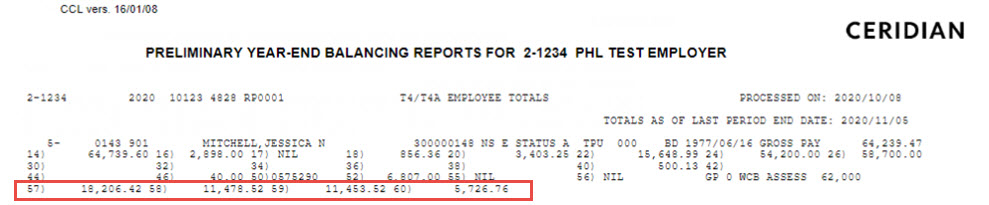

On August 26, 2020, Canada Revenue Agency (CRA) posted material introducing new T4 reporting requirements. The requirements will apply to all employers.

The 2020 T4 form will include four new Other Information Codes (57 to 60) that report subtotals of employment income (Box 14 or Code 71) paid to individuals during the following four periods based on the payment date:

-

Code 57: Employment income – March 15 to May 9

-

Code 58: Employment income – May 10 to July 4

-

Code 59: Employment income – July 5 to August 29

-

Code 60: Employment income – August 30 to September 26

Employer responsibilities

Carefully review your year-end report and preview data to ensure the amounts that are auto populated to new T4 Other Information Codes (57 to 60) are accurate.

Although every effort will be made to pull appropriate amounts paid between the dates of each period (income that would be reported to T4 Box 14 or Code 71), ultimately, it is a responsibility of the employer to perform year-end validations to avoid data errors/inaccuracies.

Please refer to the CRA website for more information: https://www.canada.ca/en/revenue-agency/campaigns/covid-19-update/support-employers-cra-covid-19.html

CRA has introduced a new form, the PD27 TWS Self-identification Form. There are scenarios offered on CRA’s website to help employers determine whether they are required to submit this form to CRA. If you need to complete this form, it is recommended that you do so prior to 2020 year-end. This will permit CRA to complete a reconciliation of the impacted account(s) and may avoid discrepancies.

You can find further information on this form here.

Instructions to help you complete this form can be located here.

The employer is responsible for determining eligibility for the income tax reduction under this subsidy program, for correctly calculating the maximum subsidy, for tracking subsidy amounts against the maximum subsidy entitlement, for retaining a record of the details of the subsidy amounts received for income tax reporting purposes and for completing and submitting the PD27 to CRA, if necessary.

- Open the COVID Wage Subsidy Report page.

Select PDF or Spreadsheet to open the report in a new window.

Select PDF or Spreadsheet to open the report in a new window. - Go to the Payroll Reports page.

- Select the Standard Reports Package for the first applicable pay period.

- ‘Gross remuneration per pay period’ - on the Payroll Register Summary, you can find this amount by locating the ‘Taxable Amt.’ below the Hours and Earnings section.

- ‘Income tax deducted’ – on the Payroll Register Summary, locate the FED.TAX amount in the Deduction Cheques Issued on Your Behalf section. Add the amount remitted to the Subsidy Claimed amount from the COVID Wage Subsidy Report to obtain the total Income Tax Deducted. If you have multiple RP accounts on the same register, you may need to add up the Fed Tax amounts for each RP account as the totals for each account need to be reported on separate PD27 forms.

- ‘CPP’ and ‘EI’ - on the Payroll Register Summary, in the Current Pay section, the Total (employee + employer portion) is the amount to be reported. Note that the sub-heading of PART TIME for CPP, EI and FED.TAX on this summary identifies CPP and EI amounts associated to the full EI rate (1.4) RP account for the payroll; CPP and EI amounts with no sub-heading are associated to a reduced EI rate RP account.

- ‘Wage subsidy claimed ($)’ - provided on the COVID Wage Subsidy Report.

- ‘Wage subsidy claimed (%)’ - to calculate this amount: divide the Wage subsidy claimed ($) by the ‘Gross remuneration per pay period’ (you found in step 3).

- Repeat steps 2-7 for each applicable pay period.

There is an Additional comments section on the PD27 where you can provide more details on how you applied the subsidy to each pay period or why you have not reduced your remittances.

Alberta Holiday Pay

Alberta recently amended certain employment and labour requirements by passing Bill 32, Restoring Balance in Alberta’s Workplaces Act, 2020 on July 29. Although there are a number of changes for employers to consider, it’s important to highlight that the holiday pay calculation changes will be in effect before Remembrance Day (November 11, 2020). Additional details are available here.

Ontario Employer Health Tax (ON EHT) deferral extension

Ontario announced that employers would have the option to defer payment of ON EHT (among other taxes). That due date has now been extended to October 1, 2020.

It is your responsibility to pay this directly to the Ministry of Finance. Payment for the previous month’s remuneration is typically due on the 15th of the following month. Example: EHT on payrolls paid in July are due to the Ontario Ministry of Finance on August 15.

Manitoba Health & Education Levy (HE levy) deferral extension

Manitoba previously announced that small and medium sized businesses (with HE Levy remittances less than $10,000 per month, with mid-month payments of tax due starting April 15) would have their payments deferred. The due date was recently extended to October 15, 2020.

Manitoba WCB

Payment can be deferred until the end of October.

Newfoundland and Labrador HAPSET

Deferred Payments are due August 20, 2020. It is your responsibility to pay this directly to Department of Finance.

Payment for the previous month’s remuneration is typically due on the 20th of the following month.

Example: NL HAPSET on payrolls paid in July are due to the Department of Finance on August 20.

Nova Scotia WCB

Deferred Payments are due October 2020.

The 10% Temporary Wage Subsidy program ran from March 18th – June 19th. The COVID Wage Subsidy page (Process > COVID Wage Subsidy) is still available for those who need to catch up on missed subsidies. You should not be using the COVID Wage Subsidy page for subsidies beyond the March 18th – June 19th program period.

On April 25, 2020, Ontario’s temporary pandemic pay program was announced as a COVID-19 relief measure. As described, the program would involve payments of $4/hour on top of regular wages and monthly lump sum payments of $250 for four months to eligible frontline workers with more than 100 hours per month. The program is intended to extend for 16 weeks (from April 24, 2020 until August 13, 2020). Support would be payable to a number of eligible worker categories at eligible workplaces and specifically excludes management. Additional details are available here.

There’s been no indication to-date that employers will need to process ON Pandemic Pay payments.

The next sitting of Ontario’s Legislative Assembly is scheduled for May 12, 2020.

Ceridian will continue to monitor for updates. We are in consultation with the Canadian Payroll Association for the most current guidance around program administration.

On April 30, 2020, Québec’s Ministry of Finance issued Information Bulletin 2020-7. It describes a Health Service Fund (HSF) credit that is available to certain employers on their 2020 HSF contribution.

The credit is available to employers that:

- are eligible for the federal Canada Employment Wage Subsidy 75% program (CEWS)

- maintain an establishment in Québec and

- have employees on paid leave due to COVID-19.

The amount of the credit is determined based on the remuneration paid to certain employees on paid leave due to COVID-19.

The credit is intended to complement CEWS and has the same three-4-week claim periods (between March 15 and June 6,2020). Remuneration paid to an employee during the claim period is not eligible for the credit if that employee had 14 days without pay during the period.

The Ministry of Finance refers to an application process for employers at the time the 2020 RL-1 Summary is submitted or a reduction of 2020 HSF contributions by the amount of the credit.

The Information Bulletin is available here.

As the COVID-19 pandemic evolves, it is critical that small businesses are equipped with the information and resources needed to support their workforce and maintain operational efficiency today and in the months ahead.

This guide is designed to help small businesses care for their workforce during the pandemic, support business continuity, and prepare for resumption of business activities.

This program and payments to Employees are managed through the CRA, not payroll:

- Go to Reports > Year-end Reports.

- Select Reports for 2019.

- Click Go.

- View Tax forms package.

- Scroll to the T4 recap report.

2020 T4 Reporting

The totals can be found on the Employee Totals page in your:

-

Preliminary Year-End Balancing Reports (go to the Payroll Reports page.

-

Year-End Balancing Reports (go to the Year-End Reports page.

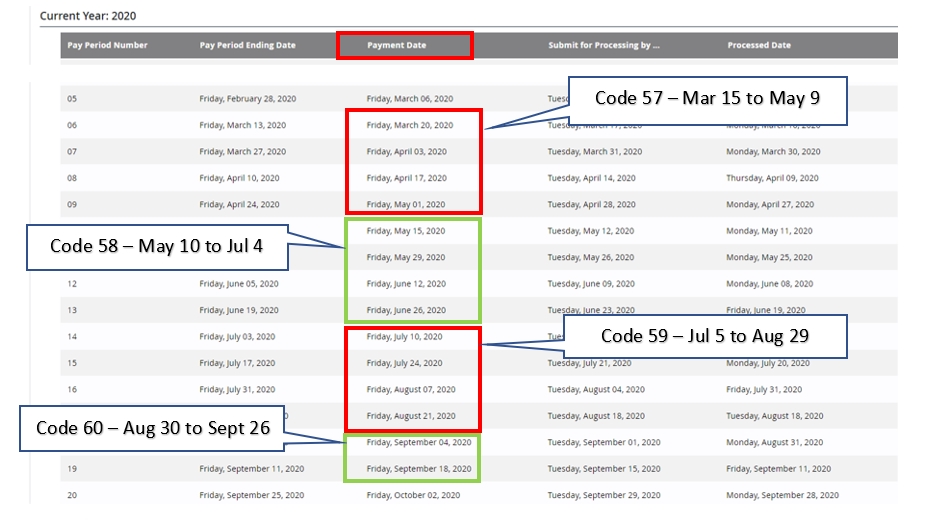

Ceridian pulled data (income that would be reported to T4 Box 14 or Code 71) based on the payrolls that ran with payment dates within the date blocks for each code period as specified by the CRA:

-

Code 57: Employment income – Date block = March 15 to May 9

-

Code 58: Employment income – Date block = May 10 to July 4

-

Code 59: Employment income – Date block = July 5 to August 29

-

Code 60: Employment income – Date block = August 30 to September 26

Important: If you processed manual cheques/adjustments, it is the pay that you entered the adjustment that determined which date block would report the income. For that reason, you may wish to review your adjustments. If the pay date and the entry date of an adjustment are in different date blocks, you can move the funds to the code period when they were paid by entering replacement amounts for the affected COVID codes on the COVID - T4 Other Information Codes page.![]() .

.

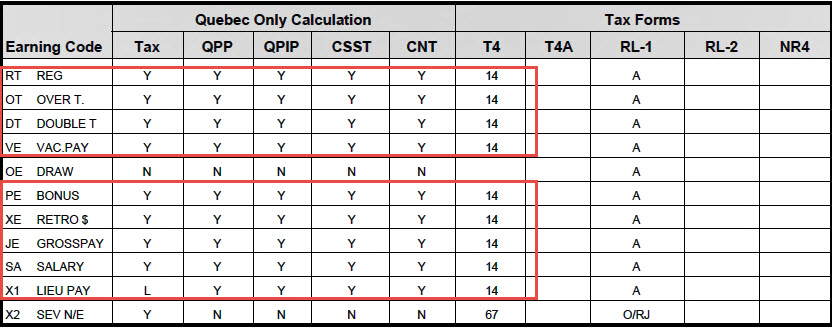

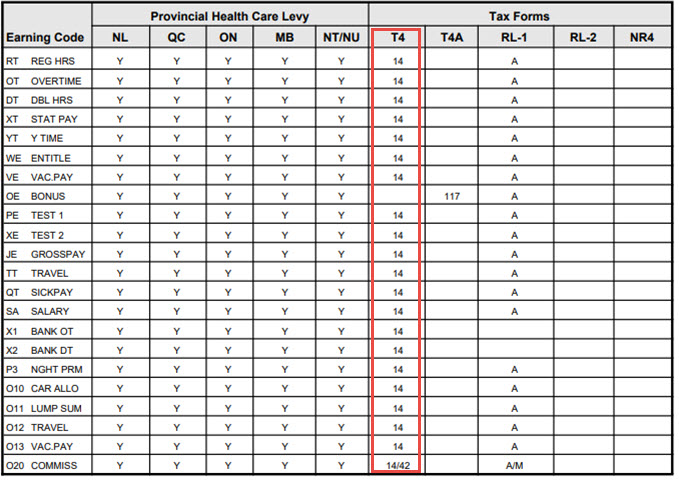

Ceridian took the earnings, deductions and taxable benefits that go into box 14 or code 71 on the T4 during the specific date blocks. Example:

Looking at your Calendar in Powerpay, we used the payment dates included in the date blocks.

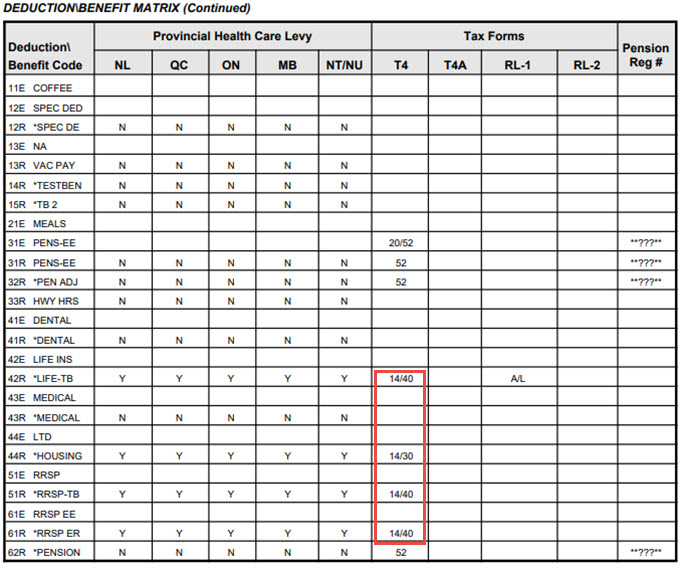

Looking at your Matrix, we took your earnings, deductions and benefits that are being directed to T4 box 14 or 71. Example: we included all the highlighted items below.

Earnings Matrix

Deduction / Benefit Matrix

Employee Reasons

If an employee was not paid during one of the date blocks, that amount will not appear on their tax form.

Employer Reasons

If you started processing payroll with Ceridian after March 15th Ceridian did not have the figures to enter into the specific boxes.

If you started with Ceridian after March 15th, 2020 and part way through a period, Ceridian did not have the per pay figures for part of the period.

You process semi-monthly with payment dates of the 15th and 30th of the month. You started with Ceridian on June 1, 2020.

| Box | Will be |

|---|---|

| Code 57: Employment income – Date block = March 15 to May 9 | 1Not appear |

| Code 58: Employment income – Date block = May 10 to July 4 | 2Incorrect |

| Code 59: Employment income – Date block = July 5 to August 29 | Correct |

| Code 60: Employment income – Date block = August 30 to September 26 | Correct |

1 Code 57 would not appear as you were not with Ceridian then and we do not have the per pay figures for those periods

2 Code 58 would be incorrect as Ceridian did not have all the required figures to complete that box

Have you processed your last pay of 2020?

-

Open a Regular or Extra Run dated in 2020. Click the Pay Period menu and click the Enter button for the pay period you want to work with.

-

Go to the COVID - T4 Other Information Codes page.

- Enter the amounts for each employee in the appropriate box.

Note: Amounts entered will REPLACE any previous amounts

Replacement values saved on this page will be processed with your last pay of the year and will be reflected on your tax forms and year end reports.

Updated Year end Balancing reports will not be generated again until after your last pay of the year is processed.

We recommend you process tax forms with the last pay of the year unless you have other adjustments that are unavailable until after January 1. The replacement values you entered will display on your tax forms as they were keyed and any remaining original values will be retained (as shown on the Preliminary Year End Balancing Report).

-

Click Save.

-

Wait until you process your first pay of 2021.

-

Go to the T4 Other Information Codes page.

-

Enter the amounts for each employee in the appropriate box.

Note: Amounts entered will REPLACE any previous amounts

-

Click Save.

You will need to add all amounts that will go into box 14 or 71 from each of the payrolls DATED within the date block for each code. For example, Code 57 would include all payrolls dated March 15 to May 9.

To determine which earnings and benefits codes are included in box 14 or 71, refer to your Earnings/Deduction/Benefits Matrix in your Year-End Preliminary Balancing Reports (Reports > Payroll Reports > Preliminary Year-End Balancing Reports) or your Year-End Reports (Reports > Year-End Reports)

Note: If looking at payrolls produced by Ceridian, refer to your Register within your Payrolls reports (Reports > Payroll Reports > Standard Reports Package) for earnings and benefits earnings.

If looking at payrolls produced by Ceridian over all date block periods, you can take the year to date figures from the pay date before the date of the block and subtract it from the pay date at the end of the block.

For example, Code 57 runs from March 15 to May 9. If your payroll is semi monthly paid on the 15th and 30th of each month (or the previous business day if it falls on a weekend or holiday), take the April 30th pay dated run year to date figures and subtract the March 13th pay dated run year to date figures to determine the amount for Code 57.

Code Date Blocks

-

Code 57: Employment income – Date block = March 15 to May 9

-

Code 58: Employment income – Date block = May 10 to July 4

-

Code 59: Employment income – Date block = July 5 to August 29

-

Code 60: Employment income – Date block = August 30 to September 26

The COVID Wage Subsidy Report page.![]() displays the details on the selections and amounts that were entered each Pay Period on the COVID Wage Subsidy page, eliminating the need to review the Audit for each pay period.

displays the details on the selections and amounts that were entered each Pay Period on the COVID Wage Subsidy page, eliminating the need to review the Audit for each pay period.

The report displays the following information when values were entered or selected on the COVID Wage Subsidy page:

-

Pay Period Number – the pay period number and run type

-

Ending Date – the end date for the pay period

-

Business Number – displays when a ‘Reduce Remittance By’ amount was entered on the COVID Wage Subsidy page for the pay period. If a ‘Reduce Remittance By’ amount was entered for multiple business numbers in the same pay period, each business number displays in the report.

-

Subsidy Claimed – the amount entered in the a ‘Reduce Remittance By’ amount on the COVID Wage Subsidy page for the business number and pay period.

-

Defer MB EHT – displays ‘Yes’ if the defer Manitoba Health & Education Levy checkbox was selected for the pay period.

-

Defer NS WCB - displays ‘Yes’ if the defer Nova Scotia WCB checkbox was selected for the pay period.

-

Defer ON EHT - displays ‘Yes’ if the defer Ontario Employer Health Tax checkbox was selected for the pay period.

The report can be viewed and saved in PDF and Spreadsheet format.

Wage Subsidy

On April 21, 2020, Canada Revenue Agency (CRA) announced that employers with a reduction in revenue due to COVID-19 will be able to apply for CEWS 75% starting on Monday, April 27, 2020. New details have been posted on the CRA site here. Included on the CRA website is an overview of the eligibility requirements and guidance on how to determine the employees/remuneration to include, how to calculate the subsidy amount (relying on a downloadable spreadsheet) and how to apply.

The CRA has posted additional information including an extensive list of frequently asked questions and a Canada Emergency Wage Subsidy application guide. For assistance with any questions in regard to completing the application, contact the CRA.

To gather any required payroll information, review payroll registers in the Reports section under Payroll reports.

If you are eligible but have not yet taken advantage of the 10% Temporary Wage Subsidy, review Powerpay COVID-19 Central for details.

To apply for the subsidy you need to file using your CRA “My Business Account” or “Represent a Client”. If you are not applying with either of those options you will need your BN and CRA Web Access code. Ceridian does not have access to this code as it is administered and maintained by the CRA. If you do not remember your code or you need a code for a new account, access the CRA Online Web access code service or call the CRA business and self-employed individuals line at 1-800-959-5525.

As an employer, you are responsible for:

- determining the eligibility for the CEWS program based on a reduction in revenues due to COVID-19,

- performing all necessary calculations and adjustments, including determining employee baseline remuneration (Average Gross Pay, below), and adjustments for employees working in related entities,

- correctly isolating the remuneration that is eligible due under the programs that are included as part of the application process,

- including in the CEWS application only the remuneration that has been paid to eligible employees,

- correctly identifying employees as arms' length or non-arm's length,

- using the CRA calculator spreadsheet and avoiding data entry or paste errors or omissions,

- determining the amount of employer-paid CPP/QPP, EI/QPIP for employees on leave with pay during the claim period,

- determining your eligible amount under the Temporary wage Subsidy 10% (TWS) program based on eligible remuneration paid during the claim period, and

- determining the total amount employees received (if any) under ESDC's Work-Sharing benefit program during the claim period.

Bill C-14, enacting the Canada Emergency Wage Subsidy (CEWS 75%), was passed on Saturday, April 11, 2020. The most current information is published on the CRA site here.

We understand that the program will be administered by CRA through My Business Account. Ceridian continues to analyze the calculation requirements set out in the bill and is seeking program clarifications through the Canadian Payroll Association and Canada Revenue Agency. We will share information and updates as they are received.

Powerpay has enhanced the new COVID Wage Subsidy page to allow you to increase the Ontario Employer Health Tax exemption from $490,000 to $1 million, if applicable.

More information is available from the Ontario Ministry of Finance here.

Please read Powerpay COVID Frequently Asked Questions.

For further information click here.

Powerpay has enhanced the new COVID Wage Subsidy page to allow you to defer your Ontario Employer Health Tax, Manitoba Health and Education Levy and Nova Scotia WCB remittances.

Please read Powerpay COVID Frequently Asked Questions.

For further information click here.

Watch this video for instructions on how to apply the COVID 10% wage subsidy, defer other provincial remittances, and and change your Ontario Employer Health Tax exemption amount in Powerpay.

Powerpay has launched a new COVID Wage Subsidy page that allows you to reduce your Federal Tax remitted in response to the 10% federal Temporary Wage Subsidy passed on March 25, 2020.

Please read Powerpay COVID Frequently Asked Questions.

For further information click here.

For further information on this program, eligibility criteria, and details on how to calculate the subsidy, review the CRA FAQ.

Ceridian will continue to support our clients impacted by COVID-19 and will assist them to implement the temporary wage subsidy recently announced by Canada’s federal government. At this time, we are awaiting more details to clarify the necessary administrative processes. Information on how to administer the subsidy has not been released at this time, however, FAQs were posted on March 20, 2020. We will release timely updates as information becomes available.

Webinars and Education

Watch to learn how to request a ROE in Powerpay and requirements needed for ROE requests specific to COVID-19.

- Webinar recording (English only)

Ceridian’s education content partners, Open Sesame and Go1, have provided COVID-19 learning materials to complement our Ceridian customers ongoing COVID-19 internal initiatives. The content being provided by our partners free of charge will be accessible for 90 days.

Click here for list of available courses and the instructions for how to access these courses in a Dayforce Learning environment that has been made accessible to all Ceridian customers.

Record of Employment (ROE)

Ceridian has been receiving calls from concerned employers on how to correctly complete Records of Employment (ROEs) for COVID-19 related absences. In particular, employers want guidance on how to complete Block 16, Reason for issuing this ROE.

Depending on the circumstances, your COVID-19 related reason codes will either be:

- A – Shortage of Work: If company is temporarily closing because of COVID-19 or parts of their business are shutting down (includes Quebec Dental Offices)

-

D – Illness or Injury: If employee has COVID-19 or if employee came back from a trip and is in quarantine

-

N – Leave of Absence: If employee is staying home because no daycare or if employee refuses to work because of COVID-19

Regardless of the reason code, in order to increase the speed of processing, do NOT complete Block 18 (Comments). Despite some uncertainty, it has been confirmed that entering comments removes the ROE from the automated process and will increase the turn-around time for claims processing.

Want to learn more?

The Canadian Payroll Association has developed Q&A with a variety of ROE scenarios for the benefit of employers as well as information about layoffs and EI benefits https://payroll.ca/.

For access to direct communications from the government, Employment and Social Development Canada has posted COVID-19 related Employment Insurance program information here.

Ceridian provides periodic and selected compliance updates that may have relevance to many of our customers. Ceridian provides this information to customers for general information purposes only. This information should not be construed as legal, tax or other advice specific to any individual or organization. Please consult your appropriate adviser for such specific advice.

For information on ROEs in Powerpay click here.

Ceridian submits this electronic file to Service Canada each business day at 1:00 pm EST. The release time of the customer’s ROE data is dependent upon the production run type.

Regular and Extra Runs

- The payment date of the production run determines when the data is released.

- The data is released at 1 PM EST one day prior to the payment date specified for the run.

ROE Run Only

The time of day when the ROE is produced determines when the data is released. If the ROE run has completed processing:

- before 1:00 pm EST, the ROE information is released at 1:00 pm EST on the same day.

- after 1:00 pm EST, the ROE information is released at 1:00 pm EST on the following business day.